– Accelerating towards Dystopia")

There is an ominous development gaining momentum across the world’s financial systems which has the potential to undermine monetary and personal freedom, yet which remains largely under the radar for most of the world’s population.

This development is the globally coordinated plan to roll out retail central bank digital currencies (CBDCs). Billed by central banks and governments as the future of money, promising benefits like payment efficiency and financial inclusion, CBDCs in reality pave the way for a dystopian future characterised by total surveillance and control, which stands in stark contrast to the principles of a free society.

At the helm of pushing this CBDC agenda are two shadowy but powerful organisations, neither of which is publicly accountable in any way – i.e. The Bank for International Settlements (BIS) known as the “the central banks’ central bank”, based in Basel, Switzerland, and the Atlantic Council, a US led, Atlantic alliance (NATO) ‘think tank’ based in Washington D.C. which is funded by a combination of government, corporate and foundation sponsors.

While the Atlantic Council pushes policy frameworks in favour of CBDCs and creates the pro-CBDC narratives, the BIS (through its ‘Innovation Hub’) coordinates with central banks in pushing the actual development and implementation of CBDCs. And in both cases, they have been very busy.

According to the 2023 BIS Survey on CBDCs in which 86 central banks participated, 94% of these central banks are exploring a CBDC.

400% Increase in Central Banks planning a CBDC

Furthermore, according to the Atlantic Council’s ‘GeoEconomics Center’, which maintains a CBDC tracker, 134 countries (which represent 98% of global GDP) are involved in, or exploring, the rollout of a central bank digital currency. Four years ago in 2020, there were only 35 countries in that same position, so you can see the huge increase in numbers of central banks involved with CDBCs over the 2020 – 2024 period.

Currently, 69 countries are in the advanced phase of readying their CBDC, a figure which covers CBDCs in the development, pilot, or launch stages. Another 44 countries / central banks are in the research stage.

Previous coverage by BullionStar in 2021 explained what CBDCs are, how they are designed and structured, and how they will facilitate surveillance and control. The links to that previous coverage are an article from September 2021 titled “How CBDCs Will Enable Surveillance & Control”, and a video from October 2021 titled “What is the Difference Between Cryptocurrencies and CBDCs?”

If you look at the above, you will see that there are 2 types of CBDC, a wholesale CBDC for use by banks and financial institutions for wholesale market transactions and things like interbank payments, and a ‘general purpose’ or retail CBDC for use by the general public that will take the form of account-based CBDCs or ‘digital cash’ tokens. It is these retail account-based CBDCs, to be issued directly by central banks, which will be programmable, and tied to user identities using Digital IDs.

The Dangers of CBDCs

From BullionStar’s previous coverage, you will also be able to see why retail CBDCs are dangerous, so we won’t go over old ground here. Suffice to say, CBDCs are dangerous digital chains for humanity because:

• With CBDCs, transactions are not anonymous, so you have no privacy. Governments and central banks can monitor every transaction and who makes it. This allows total surveillance and erases financial privacy.

• CBDCs are programmable. This allows governments and their central banks to control what goods and services a digital token can buy, to apply expiration dates on balances, and most importantly to exclude or block individuals who might criticise government policies (i.e. think Chinese type social credit score). These are all forms of social and economic manipulation and indeed economic coercion.

• For retail CBDCs to be used, they in practice require each citizen to have a Digital ID, with the CBDC account and balances linked to a digital ID. A global rollout of CBDCs will therefore a) force everyone to have a Digital ID, which b) will create a full surveillance network that tracks everyone and their financial transactions.

• Since CBDCs are issued directly by central banks, they also centralise financial power in the State and its central bank. This is highly dangerous and is the antithesis to the concepts of freedom represented by gold and silver, and the concept of decentralisation represented by private cryptocurrencies.

In summary, CBDCSs are anemia to free societies because they undermine freedom, privacy, and individual liberty and autonomy.

Just look at what the larger than life general manager of the BIS, Agustín Carstens, said about CBDCs in 2021:

Now we have this pompous authoritarian, Agustín Carstens, head of the @BIS_org.

CBDC is NOT digital cash.

“Central banks will have absolute control on the rules and regulations that will determine the use…& we will have the technology to enforce that.” https://t.co/TWEyPX8pHj pic.twitter.com/4OUMWsLS3R

— Rudy Havenstein, Senior Markets Commentator. (@RudyHavenstein) July 15, 2021

In the above clip, which was taken from a panel discussion on CBDCs organised by the International Monetary Fund (IMF) in October 2020, and moderated by the IMF managing director Kristalina Georgieva (a panel which included US Fed chairman Jerome Powell), the BIS general manager Agustín Carstens admitted that the whole reason for CBDCs is control:

“Our analysis for CBDCs in particular for the general use, we tend to establish the equivalence with cash, but there is a huge difference there. For example, in cash, we don’t know whose using a $100 bill today, we don’t know who is using the 1000 Peso bill today.

The KEY difference with the CBDC is that CENTRAL BANKS will have ABSOLUTE CONTROL on the rules and regulations that will determine the use of that expression of a CBDC [by the consumer] and also will have the technology to ENFORCE IT. Those two issues are extremely important and that makes a huge difference with respect to what cash is.”

All Major Central Banks planning a CBDC

Literally pick any central bank and country at random, and you will find that it is currently working on developing a CBDC. This ranges from the central banks of the Western industrialised Group of Seven (G7) nations of the US, UK, as well as Germany, France, Italy (as part of the ECB), and Canada and Japan, to the central banks of the large emerging markets of fellow Group of Twenty (G20) members China, Russia, India, South Africa and Brazil (all BRICS founders) as well as other G20 countries i.e. Argentina, Mexico, South Korea, Turkey, Australia, and Saudi Arabia, and the European Central Bank (ECB).

In fact, according to the Atlantic Council “19 of the Group of 20 (G20) countries are now in the advanced stages of CBDC development”.

The list goes on and on, Sweden, New Zealand, Singapore, United Arab Emirates, Bahrain, Iran, Egypt, and many manly more besides.

Here are some examples:

The Bank of England’s planned retail CBDC, which would serve the United Kingdom, is called the ‘digital pound’. The digital pound is in the design phase.

The European Central Bank’s planned retail CBDC, which would be a form of digital cash for the population of the Euro area, is called the ‘digital euro’. The digital euro has now moved beyond the design phase and is in the preparation phase.

China’s retail CBDC, which is known as the digital Yuan or the e-CNY, and issued by the People’s Bank of China, is now in the advanced pilot stage across many areas of the country.

Japan’s central bank, the Bank of Japan, is in a pilot phase with its CDBC, the ‘digital yen’.

In the US, a planned CBDC, would be issued by the US Federal Reserve, and would be known as the Fed dollar or Fed digital dollar. In 2022, the Fed issued a paper on the subject titled “Money and Payments: The U.S. Dollar in the Age of Digital Transformation“. More on the US situation below,

Singapore is planning a digital Singapore dollar in the form of both a wholesale CBDC and a general purpose retail CBDC (tokenised bank liabilities).

Russia’s CBDC, known as the digital ruble, and to be issued by the Bank of Russia, is already in the pilot phase.

India’s retail CBDC, to be issued by the Reserve Bank of India, is also already in pilot phase and already has 5 million users.

The CBDC of the United Arab Emirates (UAE), called the digital dirham, is now in cross-border testing using mBridge (more about that below), and will have both wholesale and retail versions.

Sweden’s central bank, the Riksbank, is already piloting its retail CBDC, which is known as the E-krona.

The Reserve Bank of Australia (RBA) has its CDBC, known as eAUD, already in the pilot phase.

In neighbouring New Zealand, the country’s central bank, the Reserve Bank of New Zealand (RBNZ), is at the design stage with its CBDC.

Brazil’s central bank, the Banco Central do Brasil (BCB) is in the pilot stage with its CBDC known as the digital Real or Drex.

This is not meant to be a laundry list, just a flavour to show that nearly all central banks around the world are planning to issue CBDCs between now and 2030.

CBDC Bridges

For those who believe that their own country’s CBDCs could be a dangerous tool of surveillance and control, they must also stay aware of the fact that the global plans of these financial globalists are to link all of these national CBDCs together in a global network or tightly knit mesh, that will envelope the human population. That is why you can see more and more cross-border collaboration between central banks in testing cross-border CDBC interoperability, and why the research papers of the BIS, Atlantic Council, IMF and World Bank are all pushing these cross-border ideas.

See for example, initiatives such as Project mBridge (a cross-border linkage of CBDCs involving the BIS, Thailand, China, Hong Kong,the United Arab Emirates, and Saudi Arabia), Project Dunbar (a shared platform for multiple CBDCs involving the central banks of Malaysia, South Africa, Singapore and Australia), the Digital Euro (a cross border CBDC project in its own right which is planned to be used all across the Euro area), and Project Rosalind (involving the UK and the BIS).

Denials Ring Hollow

Laughably and deceptively, nearly every central bank involved in planning to roll out CBDCs claims that they have not made any decision yet on whether to actually implement a CBDC, but at the same time they all have invested millions of dollars and manhours into creating roadmaps for investigation, design, pilot, and launch. Their denials also show that they are all singing from the same song sheet.

Some of these banks have also issued “public consultations”, but at the end of the day, it does not matter what the public consultation said or found, they are all still ploughing ahead with their CBDCs.

For example, the Bank of England states that “We haven’t made a decision on whether we will introduce a digital pound. The earliest we would issue a digital pound would be the second half of this decade.”

The European Central Bank (ECB), whose digital euro is in the preparation stage, says that “The launch of the preparation phase is not a decision on whether to issue a digital euro.”

Christine Lagarde European Central Bank (ECB) President admitted digital euro currency (CBDC) is currently planned for release in the near future & would be used in a ‘limited’ way to control the payments that individuals can make. Get caught spending over €1000 in cash… jail! pic.twitter.com/SMnIdGXUVa

— Ben Gilroy (@BenGilroyIRL) April 14, 2023

The US Federal Reserve says “While the Federal Reserve has made no decisions on whether to pursue or implement a central bank digital currency, or CBDC, we have been exploring the potential benefits and risks of CBDCs from a variety of angles”

The Reserve Bank of Australia (RBA) says that it is “examining how a CBDC could be designed and developed if a decision was ever taken to implement one.”

Even their denials use the same language of “a decision has not been taken”. These denials are actually infantile when you start to realise how this global CDBC rollout is being pushed by” behind the scenes” elites at unaccountable institutions such as the BIS, the Atlantic Council as well as at the IMF and World Bank.

Unelected Elites – The BIS

Those familiar with the gold market will already know about the opaque and ultra secretive Bank for International Settlements (BIS) in Basel, Switzerland, and how it has been involved in rigging gold prices since the 1960s starting with the London Gold Pool and continuing literally to this day. For example, see “BIS, Central Banks Are Rigging Gold Market Using Paper Gold” and “New Gold Pool at the BIS Basel, Switzerland: Part 1” and “New Gold Pool at the BIS Basel: Part 2”

The BIS, a.k.a. “the central bank of central banks,” has 63 member central banks, and its 18 member board of directors comprises six permanent representatives in the form of the governors of the central banks of the UK, US, Germany, France, Italy and Belgium, along with the governors of 11 other central banks and the ECB. The board members currently include Andrew Bailey of the Bank of England, Thomas Jordan of the Swiss National Bank, Christine Lagarde of the ECB, Joachim Nagel of the Bundesbank, Jerome Powell of the US Federal Reserve, and John C Williams of the New York Fed.

Many will also be familiar with the larger than life general manager of the BIS, Agustín Carstens, who is a former Governor of the Bank of Mexico.

The BIS is not publicly accountable to anyone, its meetings and decision making are secretive, and it does not disclose its internal discussions. The BIS even has diplomatic immunity which protects it from oversight and legal scrutiny, and it operates independent of national laws.

Since the get go, the BIS has been the guiding hand and coordinator in the global development of all of these CBDCs. This is not a coincidence, it is an agenda to bring in CBDCs across the world, with associated Digital IDs, which will also lead to the eventual elimination of cash.

Even more tellingly, in 2022 there was a bizarre article jointly written by Agustín Carstens, general manger of the BIS, and Queen Máxima of the Netherlands, titled “CBDCs for the People“, that claims that the reason to role out CDBCs is to help financial inclusion.

You might find it strange that Queen Máxima of the Netherlands is writing about CBDCs. However, this makes more sense when you realise that she is the the United Nations Secretary-General’s Special Advocate (UNSGSA) for Inclusive Finance for Development. And the UNSGSA office in New York is funded by the notorious Bill & Melinda Gates Foundation, a foundation which has been pushing for compulsory Digital IDs. When these globalists talk about broader “financial inclusion”, what they really mean is gaining total financial control over the entire world’s population.

Unelected Elites – The Atlantic Council

The other big pusher of CBDCs, the Atlantic Council, is a NATO think tank which pursues US and European cooperation on security, economic and geopolitical related issues, and is even more shadowy, but equally unaccountable, and looks like a front for the CIA, due to its board composition.

Following the money, you can see that the Atlantic Council is funded by a mix of government entities, corporations, foundations and wealthy individuals. Some of the main donors are the US State Department, the US Department of Defense, US Department of Energy, the Rockefeller Foundation, Goldman Sachs, the UK Foreign, Commonwealth & Development Office, the Delegation of the European Union to the United States, Google, the JPMorgan Chase Foundation, and George Soros’ Open Society Foundations. Other donors include Lockheed Martin, Meta, the European Union, and Bank of America.

So literally, the Atlantic Council is majority funded by entities of the US Government, the UK / EU, the Rockefellers, US big tech and big US defence sectors.

Alarm bells should ring whenever The Rockefeller Foundation and funding appear in the same sentence, especially considering their support for elements of the Covid control measures such as the totalitarian Commonpass Digital ID (along with the World Economic Forum), and the funding of Eco Health Alliance.

The chairman of the Atlantic Council is John F.W. Rogers, executive vice President, chief of staff and secretary to the board of Goldman Sachs, former under secretary of the US State Department of State and former assistant secretary of the US Treasury Department. The executive chairman emeritus of the Atlantic Council is James L. Jones, Jr. former US Marine Corps general, and former National Security Advisor to Obama from 2009 to 2010. The president and CEO of the Atlantic Council is Frederick Kempe, former editor and reporter at the Wall Street Journal.

The Board of Directors of the Atlantic Council is extensive, and includes a wide range of influential people from sectors such as US government and military. including Michael Chertoff, former Secretary of Homeland Security, Condoleezza Rice, former US Secretary of State, James A. Baker III, former US Secretary of State, Robert M Gates, former US Secretary of Defense, and Wesley K. Clark, former US Army general and NATO Supreme Allied Commander. The Atlantic Council also has many board directors from US finance and industry.

– Accelerating towards Dystopia")

Incredibly, there are also 9 former heads and former acting heads of the Central Intelligence Agency (CIA) on the board of the Atlantic Council, namely William H. Webster, Robert M. Gates, R. James Woolsey, John E. McLaughlin, George J. Tenet, Michael V. Hayden, Michael J. Morell, Leon E. Panetta and David H. Petraeus. Why is an organisation chock full of former US military and CIA heads wanting to push central bank digital currencies?

Why are the Bank for International Settlements (BIS) and the Atlantic Council so eager to jointly convince the world to embrace programmable central bank digital currencies? It’s simple, they want to use CBDCs to centralise and consolidate financial power and control over the global financial system and the world’s population.

Unelected Elites – the International Monetary Fund

The International Monetary Fund (IMF), headquartered in Washington DC, has also been pushing CDBCs from as early as 2018, and has produced a whole host of studies from “Casting light on CDBCs” (a paper from 2018), to “Cross-Border Payments with Retail Central Bank Digital Currencies” (May 2024), as well as the IMF CBDC Virtual Handbook (a reference guide for policymakers and experts at central banks and ministries of finance).

It was also in 2018 that, Christine Lagarde, the then managing director of the IMF, started pushing CBDCs at a November 2018 fintech conference in Singapore using a speech called “Winds of Change: The Case for New Digital Currency“. Exactly 5 years later in November 2023, the current IMF managing director Kristalina Georgieva, continued the CBDC push in a speech titled “The Digital Finance Voyage: A Case for Public Sector Involvement“. All singing from the same song sheet.

Not surprisingly, the IMF also collaborates with the Atlantic Council on pushing CBDCs, as this short clip below from the Atlantic Council’s president and CEO Frederick Kemp in 2022 testifies.

Today The IMF Is Showcasing A New Paper on ‘Central Bank Digital Currencies’ (CBDC’s)

In Partnership With The Atlantic Council & Several Major Central Banks…

One Step Closer To The New Digital System of Control…

The Cherry on Top of The International Surveillance State… pic.twitter.com/naPr3ZbnBu

— Spiro (@Spiro_Ghost) February 9, 2022

The Atlantic Council also less than a year ago organised a two day conference on CBDCs at the end of November 2023, with keynote speakers from, you guessed it, the Bank for International Settlements (BIS) and the International Monetary Fund (IMF). An 8 hour video of the first day of the conference can be seen here. The second day of the conference was secretive. As the Atlantic Council said: “The first day of this conference is on-the-record and open to the press. Day two will consist of private sessions and workshops.“

The Atlantic Council conference was organised in conjunction with an entity called the “Digital Dollar Project”, which was founded by J. Christopher Giancarlo, Charles H. Giancarlo and Daniel Gorfine in 2020 via a Digital Dollar Foundation. J Christopher Giancarlo served as US CFTC chairman from 2017-2019.

Not to be left out, the sister organisation of the IMF in Washington DC, the World Bank, has also been busy writing technical papers that push CBDCs, including “Central Bank Digital Currencies for cross-border payments“, and “Central Bank Digital Currency – background technical note” and “Interoperability between Central Bank Digital Currency Systems and fast payment systems”.

Another shadowy organisation based in, you guessed it, Washington D.C., that claims to be a ‘non-profit’ advocacy group is The Bretton Woods Committee. This Bretton Woods Committee’s raison d’etre is to influence the IMF and World Bank, and it too has written papers in support of CBDCs, for example, the November 2023 paper “CBDCs: Design and Implementation in the Evolution of Sovereign Money“, one of the author’s of which was William C Dudley (chairman of the Federal Reserve Bank of New York from 2009-2018).

Even more interestingly, the address of the Bretton Woods Committee is 1701 K Street NW • Suite 950 • Washington, DC 20006, which is the exact same address and exact same suite number 950 as the address of the Group of Thirty in Washington DC ( 1701 K Street, NW, Suite 950, Washington, DC 20006). The Group of Thirty (G30) is another shadowy organisation, comprising 30 of the world’s most influential central bankers and ex central bankers, one of whose members is … the Fed’s William C Dudley.

Some of the leaders of the Group of Thirty include G30 chairman, Mark Carney, former governor of the Bank of England, G30 honorary chairman Jean Claude Trichet, former president of the European Central Bank (ECB), and G30 chairman emeritus Jacob A Frenkel, who is both former governor of the Bank of Israel and former chairman of JP Morgan Chase International. Other members of the Group of Thirty include our friend Agustín Carstens, general manger of the BIS, Timothy Geithner, former US treasury secretary, Joachim Nagel president of the Deutsche Bundesbank, Andrew Bailey, governor of the Bank of England, and John C Williams, president of the Federal Reserve Bank of New York. In fact, Geoffrey Bell, the founder of the Group of Thirty, founded it in 1978 as the behest of the Rockefeller Foundation. Are you starting to join the dots?

US Republicans push back against CBDCs

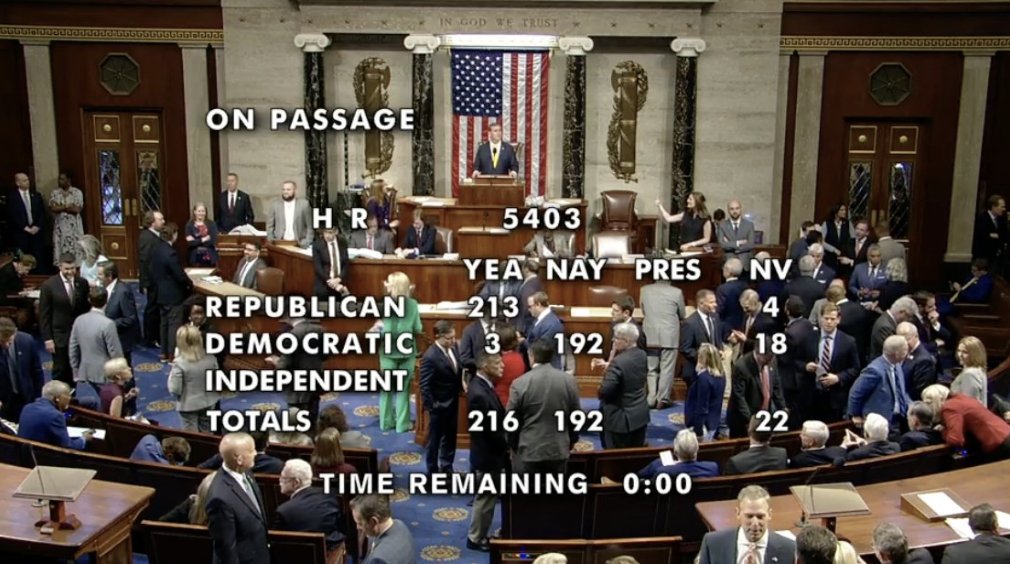

Interestingly, not everyone in the US establishment is gung ho in favour of CBDCs or a digital dollar, and some are even outright hostile. In May 2024, the US House of Representatives passed a bill that prohibits the US Treasury from creating a digital dollar without the explicit authorisation of Congress.

Officially called bill HR 5403, but cited as the “CBDC Anti-Surveillance State Act”, the bill was introduced in to the House by Republican Tom Emmer from Minnesota, and it proposes:

“To amend the Federal Reserve Act to prohibit the Federal reserve banks

from offering certain products or services directly to an individual, to

prohibit the use of central bank digital currency for monetary policy,

and for other purposes.”

The bill passed the House along party lines with 213 Republicans voting in favour and none voting against. Three Democrats crossed the aisle and voted in favour, while 192 Democrats voted against the bill. On the surface that would suggest that Republicans are in favour of financial privacy while Democrats want the introduction of a surveillance and control tool.

For more than two years, we have worked to educate, grow support, and pass this important legislation, which prevents unelected bureaucrats from issuing a financial surveillance tool to fundamentally undermine our American values.

— Tom Emmer (@GOPMajorityWhip) May 23, 2024

Upon passing, the US House Financial Services Committee issued a press release, with Committee chairman Patrick Mc Henry (Republican from North Carolina) saying that:

“This bill is straightforward. It halts unelected bureaucrats from issuing a central bank digital currency, or CBDC, that would be detrimental to Americans’ right to financial privacy.“

“We’ve already seen examples of governments weaponizing their financial system against their own citizens. For example, the Chinese Communist Party uses a CBDC to track spending habits of its citizens.”

“This data is being used to create a social credit system that rewards or punishes people based on their behavior. That type of financial surveillance has no place in the United States.“

“Concerningly, it appears the current Administration does not agree.”

“This is why the CBDC Anti-Surveillance State Act is necessary.”

“The bill requires authorizing legislation from Congress for the issuance of any CBDC—ensuring that it must reflect American values. If not open, permissionless, and private, a CBDC is no more than a CCP-style surveillance tool waiting to be weaponized.”

“I want to thank my friend, Whip Emmer, for his work to spearhead this legislation, along with Reps. Hill and Mooney for their leadership on this issue.”

In May 2023, Alex Mooney, Republican for West Virginia, has also introduced a bill called HR3712 – “The Digital Dollar Pilot Prevention Act”, which would “prohibit the Board of Governors of the Federal Reserve System and the Federal Reserve banks from establishing, carrying out, or approving a program to test the feasibility of issuing a central bank digital currency.” This bill has yet to be voted on.

Turning back to the HR 5403 bill (the CBDC Anti-Surveillance State Act), which has now passed the House of Representatives, it would still need to pass the US Senate, which does not look possible as long as the Senate is Democrat controlled, given that the Democrats are nearly all pro CBDC.

“By establishing a pilot program within Treasury for the development of an electronic U.S. Dollar, the ECASH Act will greatly complement and advance ongoing efforts undertaken by the Federal Reserve and President Biden to examine potential design and deployment options for a digital dollar.“

Conclusion

Whatever the outcome, it looks set that this CBDC issue will cause lots more debate and wrangling between US Republicans and Democrats over the months and years to come, and could even be a major policy issue to debate if the US mainstream media bothered to ask the right questions.

French Hill, a Republican for Arkansas, who Chair of the Subcommittee on Digital Assets, Financial Technology and Inclusion, had previously said in September 2023 that:

“There is no support for a CBDC in Congress, except from those on the fringes, who think that somehow a CBDC might be an amazing solution to many unstated global problems.”

It is also obvious that the push for Central Bank Digital Currencies (CBDCs) is emanating from the small network of unelected and unaccountable elites and secretive institutions that pull the levers of power over global financial policies. Major central banks, the Bank for International Settlements (BIS), the Atlantic Council, the International Monetary Fund (IMF), the Bretton Woods Committee, and the Group of Thirty are at the forefront of this behind the scenes push, and some of these institutions are funded by Anglo-American and Western governments and powerful family foundations.

It appears that because of an uninformed public and a deceptive agenda, that retail CDBCs will go ahead in many countries as central banks and governments plough ahead with their rollout with the backing of these globalist organisations. In the US the situation is less clearcut. Will the Republicans in Washington DC be able to push back against the globalist entities (some of which are ironically based in Washington DC)? Only time will tell.

One final observation. CBDCs are really the antithesis of investment gold and silver. While CDBCs are untried and untested digital expressions of decaying fiat currencies, gold and silver have been universally recognised as a store of value and have been used as money for thousands of years.

Gold and silver have intrinsic value and offer privacy and anonymity in transactions, with no digital footprint. When you own gold and silver you are ringfenced from the financial repression of central banks and their monetary system.

In contrast, CBDCs are issued and controlled by central banks and CBDCs are programmable. By definition CBDCs allow centralised control by the issuer, and also CBDCs are designed to collect data on accounts and balances, so they are susceptible to surveillance and privacy invasion. CBDCs can also be used for confiscating money as they can force use of a programmable currency which can be switched off and have conditions on spending imposed as well as programmable expiry dates. Gold and silver have none of these drawbacks.

While physical gold and silver represent economic freedom and liberty, Central Bank Digital Currencies (CBDCs) represent slavery and a dystopian future.